NQ vs MNQ: Differences and Which One You Should Trade

Same index, same chart, same setups. The only thing that changes is how many dollars each point is worth. That's the whole answer. Everything below is why, and where the line actually sits.

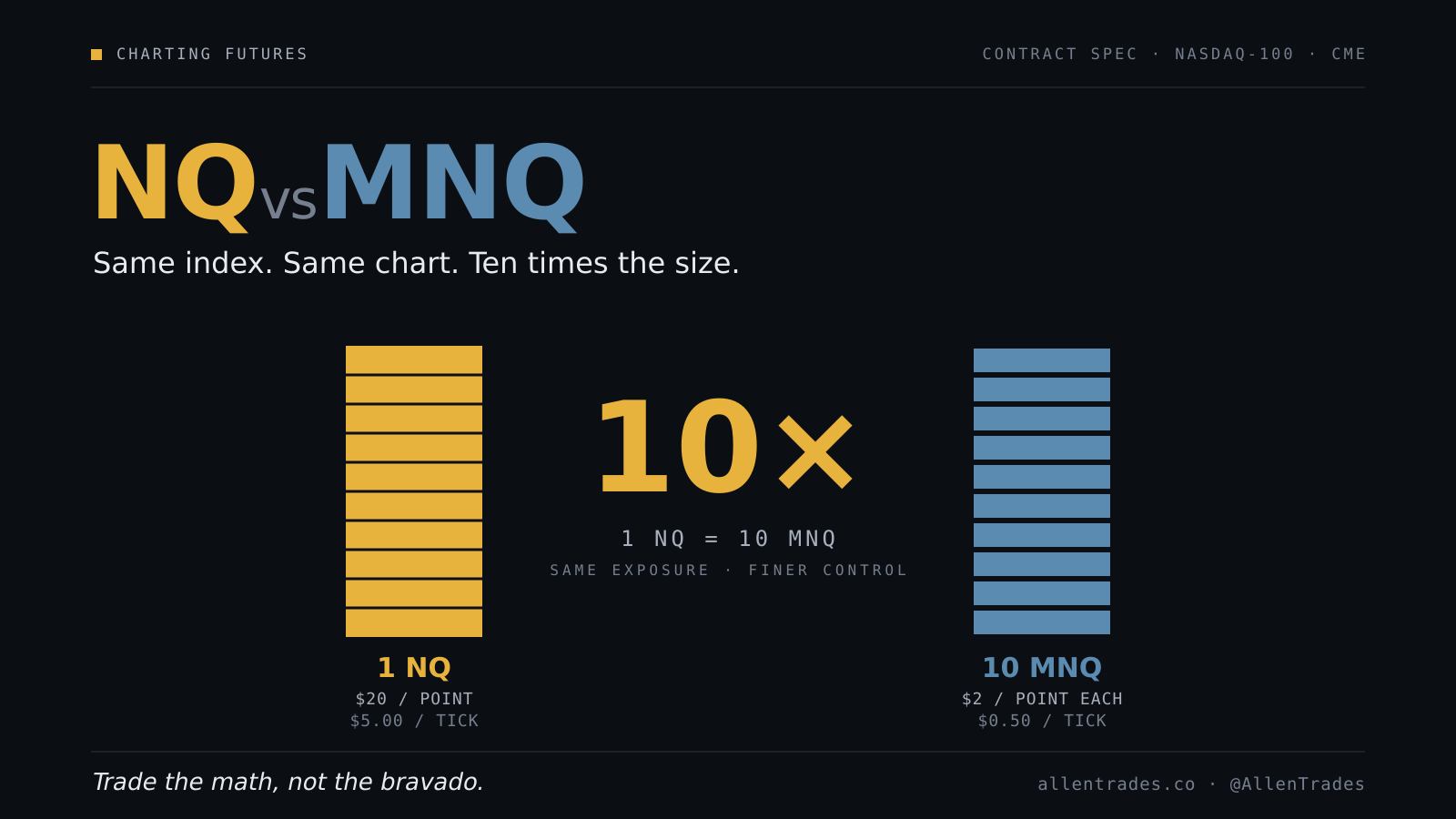

They are the same thing at different size

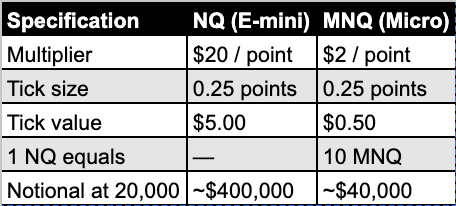

NQ is the E-mini Nasdaq-100. MNQ is the Micro, launched in 2019 at exactly one-tenth the size. They track the same index, tick for tick, in the same direction, at the same price. Your structure read doesn’t change. Your entry model doesn’t change.

What changes is the multiplier. NQ pays $20 a point. MNQ pays $2 a point. One NQ contract is ten MNQ contracts. Nothing else.

Tick and point values

A 25-point move is $500 on one NQ. The exact same move is $50 on one MNQ. That’s the entire difference, and it’s the only number that should drive your decision.

Margin is not the deciding factor

Margins move with volatility and vary wildly by broker. Roughly, NQ runs you somewhere in the high four figures to low five figures of initial margin at the exchange level, with day-trade margins as low as a few hundred bucks at some firms. MNQ is a tenth of that, with intraday margins sometimes under $100.

Don’t size off margin. Day margin tells you what a broker will let you hold. It says nothing about what you can afford to lose. Plenty of blown accounts had margin to spare. The number that matters is risk per trade.

The real decision: risk-per-trade math

Here’s the only calculation that matters. Take your dollar risk per trade. Divide it by your stop in points times the multiplier. That’s how many contracts you can hold inside your rule.

Risk $200, 25-point stop:

NQ: 25 × $20 = $500 per contract. $200 ÷ $500 = 0.4 contracts. You can’t trade NQ here without breaking your own rule. Trade MNQ.

MNQ: 25 × $2 = $50 per contract. $200 ÷ $50 = 4 contracts. Clean. You hold 4 micros and you’re inside your number.

If your risk budget can’t cover even one full NQ contract at your normal stop distance, you have no business in NQ yet. You’d be forced to either skip the trade or over-risk it. Both are mistakes. MNQ exists exactly so you don’t have to make that choice.

When to graduate from MNQ to NQ

You graduate when one NQ contract fits comfortably inside your risk per trade, with room to spare.

Risk $600, 25-point stop:

NQ: 25 × $20 = $500. $600 ÷ $500 = 1.2 contracts. One NQ ($500 risk) now fits with cushion. You’ve cleared the bar.

That’s the line. Not your account balance, not your ego, not how long you’ve been trading. The math. When your per-trade risk clears the cost of one NQ at your real stop distance, you can step up. If you want the precision back, run 1 NQ plus a couple of MNQ to fine-tune. Nothing stops you mixing them.

And here’s the part most people skip: graduating doesn’t make you a better trader. It just makes every mistake ten times more expensive. The setups are identical. If you can’t run MNQ profitably, NQ won’t save you. It’ll just bleed you faster.

Bottom line

Pick the contract that lets you take your normal setup at your normal stop without breaking your risk rule. Under $25k or sizing in small increments, that’s MNQ. Once one NQ clears your risk per trade with room, you’ve earned the size. Same chart either way.

Trade the math, not the bravado.